Eliminating waste through Lean principles means balancing tradeoffs.

Practitioners of Lean manufacturing are familiar with Taiichi Ohno’s seven deadly wastes: overproduction, waiting, transportation, inappropriate processing, unnecessary inventory, unnecessary or excessive motion and defects. While focusing on waste elimination in each of these areas is desirable, often dealing with production realities means tradeoffs must be made.

As a result, reducing costs by improving efficiency drives manufacturing and quality engineers to become combinations of risk analysts, strategic planners and coaches. This is because all wastes tie into one another and reducing one may fix others. So, the most effective Lean strategies look at the overall organization and the way each action impacts other actions. A robust Lean program emphasizes to each employee that customers include both the party receiving the product and the person who touches a product after they finish processing it. The result is an organizational culture that focuses on improvement, but also recognizes constraints.

Cause and effect. Nowhere are constraints more evident than in the electronics manufacturing services environment. Even when customers are targeted based on their maturity in Lean practices, variations in forecasting, processing and supply chain are introduced with every new customer. This month, we look at each of the seven wastes and likely tradeoffs that must be considered. We also look at practices EPIC has found successful in achieving balance between Lean best practices and the reality of serving a diverse customer base.

Overproduction is a waste typically driven by inefficient processes and as such, it often reflects elements of the other six wastes. Overproduction results when inefficient processes drive higher scrap levels or shortages, and production output is increased to ensure demand is met. Automation is one way to increase production efficiency and quality, but EMS automation strategy needs to be flexible to support likely variations in product configuration and demand. Higher levels of automation can also drive higher cost, so the “perfect” level of automation may never be achievable. Plus, automation is only half the equation. Preventive maintenance and calibration are important in ensuring repeatable processes, as equipment that fails or is out of spec will add bottlenecks or defects. Smaller lot sizes can help minimize overproduction, but every changeover introduces an opportunity for failure and decrease in operational efficiency.

EPIC’s model looks at automation strategy carefully. Equipment and process variation is minimized. The same platform is used in all facilities, so improvements made in one facility are easily transferred. Specialized wave solder equipment and vapor phase reflow are used to create a broader process window that either permits automated changeover or doesn’t require any change between products. All SMT lines are identical. There are no specialized topside or bottom-side lines.

Production personnel are cross-trained in multiple processes so they can move between processes based on demand patterns. Smaller lot sizes can be processed with minimal changeover impact, and demand variations driven by multiple customers are accommodated with minimal waste of resources or bottlenecks. Design for manufacturability/testability (DfM/DfT) recommendations help guide customers toward practices that better utilize production resources and minimize defects. The effect is minimized overproduction.

Waiting is a simple waste. Products in wait state at any point in production are essentially stagnant money merely sitting on the floor. Increasing throughput by processing in smaller batches converts waiting to free cash. However, elimination of waiting is achievable only if material is available. A single, inexpensive passive component delay can halt a production build, negatively impacting inventory turns and cash flow.

EPIC’s system typically processes product into finished goods within 48 to 72 hr. Material bonds are established and buyers are focused not on ordering to JIT demand, but on managing exceptions down the pipeline. The result is the ability to identify potential material shortages with long enough lead-time to address the issue. The DfM/DfT discipline, broader process windows and smaller lot size philosophy described above also contribute to reduced bottleneck potential and an overall reduction in wait time between processes. The net effect is improved inventory turns, increased cash flow, and improvements to on-time delivery.

Transporting is the waste of excessive movement. Transport waste can be created in many ways. A poorly laid out facility is often the biggest driver of transport waste. However, inefficient automation or too much process segregation can also drive this waste.

Our factories are designed to minimize transport by moving production in a synchronous manner according to general processing requirements. Where possible, multiple processes are combined both to eliminate transport waste and potential defects that can be introduced in isolated processes. For example, in some build-to-order projects’ final programming, test and packing are combined at the test station. This minimizes transport between workstations, eliminates the possibility that varying configurations will be mislabeled, and optimizes process takt times to improve product flow.

Inappropriate processing is waste driven both by lack of DfM/DfT discipline and by lack of sufficient documentation control. This can be a more difficult waste to control in the EMS environment because customers may reject DfM/DfT recommendations, and robust documentation requirements can create bottlenecks. EPIC’s DfM/DfT system prioritizes recommendations to make it easier for customers to understand how critical each recommended design change is to overall product quality. Documentation control is centralized to make sure production only has access to the most current revision of work instructions. Design travelers accompany each work order to ensure that during shift changes or personnel changes there is a clear trail on what is being processed. Smaller batch sizes also contribute to minimizing this waste.

Unnecessary inventory is also a challenging waste to minimize in the EMS environment. Unnecessary inventory comprises raw material, work-in-process and finished goods inventory. While smaller lot sizes can minimize WIP, the relationships with customers found in EMS means forecasting and supply base choices are often a compromise between customer preferences and Lean best practices. Economy-driven variable demand further tests the system.

In the EPIC model, the program manager starts by developing the customer order replenishment methodology. The tool for determining visibility into the customer’s demand is defined (i.e., ERP, EDI, etc.), and replenishment “pull” signals are defined.

Once these issues are addressed, initial finished goods kanban bin sizes are established. Trends are analyzed and bins resized as appropriate with customer approval. Strategic suppliers produce to the MRP forecast and ship to EDI release signals. Consignment, in-house stores and vendor managed inventory programs are used with strategic suppliers to maintain buffers closest to the point of use.

Pipeline status or “bond” reports are regularly reviewed with supplier teams to ensure buffers and replenishment streams are able to support planned production within a range of variation based on past historical demand, current forecasts, customer service lead-time guarantees to their end-market, manufacturing lead-times and transit lead-times.

Like the wastes of transport and inappropriate processing, unnecessary or excessive motion costs money and slows throughput. And, as with the waste of inappropriate processing, customer reluctance to implement DfM/DfT recommendations can be a constraint in improving efficiency.

EPIC’s automation strategies, DfM/DfT process and focus on designing factories with sequential processes all help improve efficiency, but ultimately, the most success in reducing this waste comes when customers are willing to adopt DfM/DfT recommendations. Engaging the EMS provider during the design stage ensures optimal process efficiencies, translating to a successful and cost-effective product launch.

Excessive defects represent both the seventh waste and a byproduct of most of the other wastes. They drive unnecessary inventory and overproduction. However, completely eliminating defect opportunities carries a high cost, and most EMS providers make tradeoffs to minimize defects while aligning with customer cost goals. Other defect minimization practices include:

Eliminating non-value-added activities.

Minimizing touch labor.

Maintaining a well-trained workforce.

Using Six Sigma tools to analyze root cause of defects.

There is no one right formula for eliminating any of these wastes. The best course is developing a strong production framework with processes that accommodate the bulk of customer requirements, and fine-tuning as required.

Ryan Wooten is engineering manager at EPIC Technologies (epictech.com); This email address is being protected from spambots. You need JavaScript enabled to view it..

Shipments and revenues should skyrocket in 2010, leaving the spectres of 2009 behind.

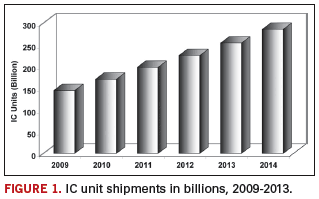

IC revenue will stage a comeback this year, growing 18.8%, with unit growth a tick lower at 18%. Both figures are considerably better than the 8.8% decline in revenue and 6.9% decline in shipments in 2009.

DRAMs are anticipated to be the largest growth area for ICs, with revenues up 40% in 2010. Numerous analog chips, including regulators and references, computer, communications, automotive, and industrial applications; special purpose logic chips, including consumer, computer, communications, and automotive; flash, EEPROM, 32-bit MCU, and standard cell and PLD chips will see revenue growth rates in excess of 15%.

Shipments should continue to climb at least through 2013, according to NVR data. Unit growth should top 100 billion over the four-year span of 2009 to 2013 (Figure 1).

What’s driving the recovery? Low interest rates, low oil prices, and the stimulus packages instituted around the world are all contributing to a stabilizing economy and upturn. Purchases were less than the replacement market in 2009, and pent-up demand is pulling the market in a positive direction.

Cellphones, particularly high-end smartphones, will see high growth rates. Smartphones are gaining in popularity and becoming a larger piece of the cellphone pie. Anything handheld and somewhat affordable that keeps us connected to the rest of the world seems to be doing well. New product introductions such as Apple’s latest iPhone are hot topics; the iPad is expected to do well, and Research in Motion’s Blackberry has been doing well for some time.

Netbook computers, with prices as low as $200 during holiday sales, and notebook computers are driving up IC demand. Other high growth areas include 3-D and digital TVs, DSL/cable modems, flash drives, memory cards, set-top boxes, digital cameras, automotive, and an assortment of audio applications.

The economy is stabilizing, which is easing fears of spending on consumer goods. The housing market, which took down the economy by taking the credit markets with it, is stabilizing, and the ratio of income-to-housing expenditures is more balanced than it was previously.

The automotive market, host for numerous ICs, fell substantially during the downturn. This market did benefit from the cash-for-clunkers program, although automotive sales receded again after the program ended. But it became a booster to spending, which helped. And automotive is expected to turn up in 2010 and beyond, particularly in areas such as China. Overall, spending is higher now than it was in the depths of 2009, and that is what is pulling us up and out of the sloth of 2009 and will carry us to a more positive future.

Sandra Winkler is senior industry analyst at New Venture Research Corp. (newventureresearch.com); This email address is being protected from spambots. You need JavaScript enabled to view it.. This column runs bimonthly.

Our newest columnist seeks to expose the synergy of fabrication, assembly and end-use.

Hello! I’d like to take a few moments to introduce myself, though I feel like I have known most of you for years. I have the opportunity to write this column as a result of my predecessor, John Swanson, moving on to smaller and more expensive things. John has taken the task of expanding our business to include electronic packaging. After 10 fast-paced years in the industry, I now find myself managing a business unit.

A little about me. I love yoga. It never allows my mind to travel to the pressures or issues encountered in life. But what I enjoy most is that I usually feel like a superhero after the class is completed. This last time, though, there was a new instructor, who began the class by saying, “Tonight we are going to concentrate on the basics.” Great, I thought. How can I reach superhero strength if we are going back to the beginning?

Yet, I left an extremely sore and beaten woman. Not only was I a better person than the one who entered, but I had my idea for this column: How can we expect greatness if we do not pay attention to the basics?

It’s cliché, but building a strong foundation paves the way for success in everything we do. Consider process control. Again, I know part of you is cringing, but there is another side that remembers the last three product issues experienced came down to poor process control. Ensuring good control will result in the best possible products we can make.

Did you know that when the board goes through the reflow oven, if vias are not properly plugged with soldermask, the mask cracks, leaving exposed copper? As in Figure 1, the copper found through the crack has not seen any protective coating and becomes a breeding ground for corrosion. If soldermask registration is off on a pad, and the solder cannot collapse properly, the resultant joint is more susceptible to thermal fatigue.

Imagine a BGA pad that has one side soldermask-defined, as a result of misalignment, and the other metal-defined. The solder collapse will not be uniform. During reflow, the soldermask will expand on the one side, creating pressure on the sphere, which acts as a lever. This can promote joint cracking.

Inadequate copper preparation will result in nonuniform coverage of an OSP coating. This is true for all surface finishes, though shortcuts often are taken at the cleaner and microetch steps of a process. If the copper surface has contaminants, the finish will not properly bond to the copper. This can manifest itself as nonuniform coverage, poor surface coating adhesion, insufficient thickness, solder joint voiding, and even premature tarnishing.

Also true for any surface finish is the importance of coating thickness. Believe it or not, thickness specifications were put on the technical datasheets for a reason. The specified thickness is critical to the coating’s performance. Everyone has experienced an insufficiently plated tin deposit. After one reflow, all the pure tin had been quenched by intermetallic that laughed at you on the second assembly pass.

Focusing on process flow and routine analysis can eliminate many future quality issues. Did you know sending a board twice through Pb-free HASL can embrittle the soldermask to the point where the resultant product will have much worse creep corrosion than any thin immersion silver deposit? Did you know the first instance of soldermask interface attack on an immersion silver board was found as a result of a customer continuously dragging microetch into the following rinse, which did not have a sufficiently strong turnover? Basically, the PCBs were being double-etched, and then put directly into the pre-dip bath.

On a positive note, running the right process controls can make a better product. Choosing the proper equipment for immersion tin can minimize solution air exposure and extend bath life. Premature tin oxidation and thiourea decomposition can be greatly reduced. Using the right pre-clean, including a well-maintained microetch, can enhance the OSP and immersion silver coating quality, which in both cases enhances solderability.

Maybe you do realize all this. But did you realize how much research at a chemical supplier goes into widening an operating window to accommodate the “what ifs” in fabrication? It is amazing what is asked of the surface finish on a day-to-day basis.

I don’t want this to be a finger-pointing exercise. I want to provoke thoughts on how to make process control second nature. I want to expose the synergy of the fabrication, assembly and end use performance. Every detail affects the next step and ultimately the final product.

When I started on this journey, I learned quickly that there was an application for each surface finish. They all have strengths and weaknesses. If processes are run according to specifications provided, and the same can be said for the processes around them, the resultant product will be superior. There are many instances where a coating outperforms the expectations of the chemical supplier, fabricator assembler and end-user. Imagine a surface finish produced as a result of everything run under optimal conditions: superhero status.

Lenora Toscano is final finish product manager at MacDermid (macdermid.com); This email address is being protected from spambots. You need JavaScript enabled to view it..

Will companies in the land of key suppliers remain powerhouses?

While much of Asia is recovering from the economic downturn, Japan still struggles. While some improvements can be seen, a difficult road is ahead. According to Japan’s Cabinet Office, the nation’s economic composite index rose 1.6 points to 95.9 in November, gaining ground for the eighth consecutive month, on a production recovery driven in part by China’s economic growth. This marks the first time since 1997 the index has moved up eight months in a row, prompting the Japanese government to state for the second straight month that the overall economy is improving. Manufacturers’ output continued to increase, with the industrial production index rising 2.6% and shipments of producer goods climbing 1.6%. Large-scale power usage grew 2.2%, signaling that factory-operating rates are improving. Sales in wholesale trade were also strong. However, the composite index was still below the levels seen before the financial crisis erupted in autumn 2008, and domestic demand remains sluggish. Sales for small and midsize manufacturers slipped 1.2% in November. According to BNP Paribas Securities (Japan) Ltd., real GDP growth will likely be 4% for the December quarter. While Japanese GDP still places it as the second largest economy in the world, the country may not be considered the economic powerhouse that it once was. Toyota’s massive recall is the latest blow to the Japanese corporate image, at least for that of quality. The country is a far cry from the days back in 1989, when the late Sony founder Akio Morita and politician Shintaro Ishihara published the famous The Japan that Can Say No.

Will companies in the electronics industry remain powerhouses? The recent Global Semiconductor Packaging Materials Outlook, published by SEMI and TechSearch International, revealed that Japan-headquartered companies hold major shares of the semiconductor packaging and assembly materials business. Ibiden and Shinko Electric are the two top laminate substrate suppliers in terms of revenue. Japan-headquartered suppliers dominate the global leadframe market, holding more than 50% in revenues of the 2009 market. Japanese mold compound suppliers accounted for greater than 70% of the global mold compound market. These companies include Hitachi Chemical, Kyocera Chemical, Nitto Denko, Shin-Etsu Chemical, and Sumitomo Bakelite. Japanese companies such as Shin-Etsu and Namics are also major underfill material suppliers. In die attach paste, Japanese companies hold a smaller share, but in die attach film, Hitachi Chemical dominates the market and Nitto Denko is also a key player. In solder spheres, Senju Metal Industry has maintained its leadership position for many years. Many of these firms have been a great source of new material developments critical to our industry. While no one expects another plant explosion that cuts the world’s supply of a material, such as the one that took out one of Sumitomo Bakelite’s mold compound plants many years ago, it is critical that materials research continues to meet the industry’s evolving needs. As the industry moves into the next silicon technology nodes and ultra low-k dielectrics, new material development to meet packaging needs will be critical.

Unprecedented unemployment. Major Japanese companies are going through a period of layoffs not seen since before World War II. With recent changes in Japanese law regarding the use of temporary and part-time workers, large Japanese companies are not only closing plants, but are shedding large segments of their workforces. Even Japanese subsidiaries of multinational companies have closed operations, such as the closing of Nokia’s R&D center in Japan, which put approximately 200 researchers out of work. All these practices have created a large number of “consultants” available for hire – a development that may be beneficial to overseas companies seeking assistance gaining greater understanding of business practices and means to better penetrating Japanese markets.

What does the future hold for Japanese electronics companies? Will they still be able to maintain the strong commitment to R&D in electronic materials and other areas? Will the latest mergers between companies such as NEC and Renesas result in a stronger, more able electronics company? What future mergers can be expected? A prediction: Japanese companies led by “maverick” thinkers in executive roles will be the ones that prosper. The fate of Japanese corporations that do not evolve to meet the new economic challenges is uncertain. CA

References 1. Nikkei, Jan. 9, 2010.

E. Jan Vardaman is president of TechSearch International (techsearchinc.com); This email address is being protected from spambots. You need JavaScript enabled to view it.. Her column appears bimonthly.

Research continues on improving printed frontside silver conductor line efficiency.

A simple Internet search will reveal the photovoltaic industry is working hard on higher aspect ratio frontside conductor grids as a route to greater solar cell efficiencies. This is because the conductors, typically screen-printed on a cell’s frontside, block sunlight from reaching the energy converting strata below, and the narrower they are, the less shadow they cast.

However, as it is essential they maintain their current carrying capacity, and as this is governed by their cross-sectional area, it follows that as their width decreases, their height must increase. Hence the need for a greater height/width ratio, or aspect ratio.

While the pursuit of higher aspect ratios is essential, this goes hand-in-hand with an equally important factor that until now has been largely overlooked: conductor uniformity. This will become a critical factor as feature miniaturization progresses, as a conductor with many high/wide and low/narrow points is less efficient than one that has the same cross-section throughout.

A team here has been conducting in-depth studies on this issue since 2008, with the aim of developing a method for improving the efficiency of printed frontside silver conductor lines. Recently, results of this ongoing work were presented at the 24th European Photovoltaic Solar Energy Conference in Hamburg.

As part of the study, the team looked at the relative merits and demerits of printing using conventional mesh printing screens versus two-layer electroformed nickel stencils, carrying out extensive tests on both to identify the features necessary for an optimized, high-aspect ratio printing process.

They also explored in detail a significant obstacle to achieving the improved levels of paste transfer efficiency required for higher aspect ratio conductors when printing with conventional mesh screens: The screen apertures are partly full of wire. The first problem is the volume of screen aperture occupied by the wire cannot be filled with paste; and, second, the wire presents a large surface area to which paste can stick instead of transferring to the wafer.

Indeed, when analyzing conductor structure, it was graphically clear that the intervals between the highs and lows in any conductor mirrored the intervals between the knuckles in the screen mesh.

Much has been done to mitigate this problem. Wire diameters have been reduced to a current industry standard of 20 to 25 µm, and this has greatly improved aspect ratio and conductor uniformity. However, there is a limit to how fine a wire can be used, especially considering a screen must be sufficiently robust to withstand 10,000 sweeps of a high-speed, high-pressure squeegee. There is also a cost issue: Fine, high mesh-count screens are more expensive than large diameter, low mesh-count screens.

One obvious solution is to remove the mesh from the apertures completely, and several successful attempts already have been made to do just that using two-layer electroformed stencils. Our team decided to explore this option using a number of high-precision, two-layer electroformed nickel stencils designed especially for the tests.

Two-layer stencils typically use a bottom nickel aperture layer in which the wafer pattern is formed. This is protected and stabilized by a top layer, which, in its coarsest form, is a simple perforated foil. Such stencils provide much improved paste transfer and conductor uniformity over mesh screens, but improvements can be achieved by replacing the standard perforated foil with one that has reinforced apertures similar to, and that correspond with, those in the bottom layer. Here, the challenge lies in precisely aligning the two layers, and in ensuring the apertures are well-engineered.

Using appropriate pastes and this more sophisticated approach to stencil design, improved aspect ratios were achieved, as line widths were decreased to 50 µm and conductor uniformity was significantly better than anything realized using mesh screens.

Given these results, the team noted two-layer metal stencils could potentially outperform the best emulsion mesh screens, but that several obstacles must be overcome before this technology can be implemented widely. First, whereas the photoimageable emulsion used for mesh screens is sufficiently elastic to provide a reliable gasket between the screen and the wafer’s textured surface, the bottom layer of a nickel stencil is unyielding and could cause silver paste to bleed, creating more problems than are solved. Also, the stencil’s bottom surface must be totally defect-free; nickel nodules could crack or even break the wafer as pressure is applied. Such stencils are also more expensive, and their use in high-definition work requires a high degree of technical skill.

Having said this, electroformed stencils do provide relatively open apertures. This, and the considerable advantages of mesh screens, led the team to develop a third option: a hybrid solution based on a conventional screen, but that replaces its wire mesh with a prefabricated electroformed nickel top layer with reinforced apertures similar to those used in two-layer electroformed stencils. This is coated on the underside with traditional photoimageable screen emulsion, enabling the team to maintain the ”soft contact” gasketing properties of screen emulsion while freeing the apertures considerably.

Details regarding a hybrid screen solution were presented at the Hamburg event. This hybrid technology is effectively a printing screen with almost no metal in the apertures that, once its design is optimized, should offer better paste transfer efficiency, aspect ratio and cross-sectional area uniformity than the alternatives from which it is derived. CA

Tom Falcon is senior process development specialist at DEK (dek.com); This email address is being protected from spambots. You need JavaScript enabled to view it..

Switching from a single offering to end-to-end involves breaking down certain internal barriers.

Everyone knows it’s an outsourced world. So how to compete? How about integrating vertically?

Good reasons abound, but first and foremost, integrating is a response to existing customers’ needs. The vertically integrated supplier transcends the mundane to become a key factor in its customers’ success. Generally, too, it appeals to a broader base of prospective customers, allows outsourcing trends to be fully exploited, creates revenue and margin opportunities, and changes the scope of competition.

Formed in November 2002, upon its divestiture from IBM’s Microelectronics Division, Endicott Interconnect offers end-to-end electronics packaging and production, from semiconductor package design and fabrication, to laminate development, bare board fabrication, component assembly, test, and box-build. It takes a lot of space and a lot of manpower to do all this well (in our case, 1.4 million sq. ft. and more than 1,600 employees), and we’ve enjoyed a good run after a challenging start as a brand new company.

Now our model evolves. Through the IBM years, we were a manufacturer of components and an integrator of systems in the form of capital equipment. Newly formed EI focused strictly on manufacturing components. Today, we manufacture components while simultaneously growing a systems integration business in which we move backward toward the bare die and forward toward direct fulfillment.

Along the way, we’ve learned that the more you offer, the more credentials are necessary. (In our case, the list includes AS9100, NADCAP, ISO 13485, ITAR, among others.) We recognized the need to spend money on people, equipment, facilities, and capabilities (capital spending hovers around 8% of annual revenue, and our R&D budget ranges from 2.5 – 4.5%). We learned to build incrementally on existing talents. And we aggressively sought ways to do more for every customer.

To extend our reach first meant recognizing the limitations of our structure. Silo organizations were built around business units (component substrates, printed circuits, printed circuit assemblies), with conflicting objectives among units. When it came to competing for resources, a certain selfishness prevailed.

To tackle the problem, we unified the business units under a single management team and hired staff with skill sets the organization lacked. This also meant shedding workers who would not, or could not, support the changes that had to be made.

Concurrently, we remodeled existing space to establish premier manufacturing facilities. We allocated capital to increase capacity and improve capabilities, specifically focusing on capabilities that would enhance the vertical integration strategy. For instance, we acquired eV Products (now eV Microelectronics). The CZT crystal technology we gained with the acquisition is used in sensing applications in medical and homeland security applications – two market segments that are integral to our strategy. We added staff with program management skills. And we sought synergies with public and private sector organizations to leverage resources, exemplified by the Center for Advanced Microelectronics Manufacturing on our campus.

‘Brainpower as a differentiator.’ Besides bringing in talent to plug identified gaps, we also redoubled our efforts to use existing in-house expertise. We had an R&D group with over 800 career patents. We began to focus its efforts on customer problems – whether materials, processes, or systems. Sometimes we ended up developing new processes and materials where commercially available ones were inadequate. In short, we profited by putting our technical experts face-to-face with our customers. Where some companies tout their pricing or global reach, we used brainpower as a differentiator.

Meanwhile, we set about penetrating the customer on every level. Within our sales and marketing organization, we built skill sets compatible with selling broader capability. The vertically integrated company sells more than a single widget or service, so it must look deeper and wider at what the customer is doing and what they need. Ask: What more can I do for you? How can I show you? Then blow your own horn, often and loudly (this column is one example).

It takes bench strength to win big end-to-end programs. We hired electrical designers and software engineers, added system architecture expertise, applied our expertise in hardware design (substrates, power, cooling), and figured out how to cost and price all these new things. Through it all, we learned to collaborate both more often and to a greater degree with customers and other organizations.

Moving from a single product or service to a vertically integrated model requires constant focus on how to make your company more attractive to existing and prospective customers. At the same time, however, it means keeping an eye on the ground to avoid pitfalls that come with doing multiple new things simultaneously.

Make use of the underutilized talents of your staff, and plan on hiring and firing, too. The transition requires collaborations, partnerships, and, yes, spending, but the payoffs can be huge. CA

Rex Green is global sales manager and product manager at Endicott Interconnect Technologies (eitny.com); This email address is being protected from spambots. You need JavaScript enabled to view it..