Charles Robert Darwin communicated his theory of evolution more than 150 years ago. He observed some unique zoological evolutions while visiting the Galapagos Islands in Pacific Ocean during a global circumnavigation on a British research vessel name Beagle. Darwin recognized that each isolated island experienced its own evolution; each species developed a unique trait specific to that island. Darwin’s Theory of Evolution grew from these observations.

Component Placement “Two Worlds Converging: Chipshooting and Flip-chip Bonding” Authors: Eric Klaver and Patrick Huberts Abstract: Pick-and-place equipment has over the years mostly evolved in four key areas: It is faster, more reliable, more accurate and more user friendly. Most pick-and-place vendors have aimed at the mass production market, while others have moved toward more dedicated markets – mostly where production flexibility is needed, as with high-mix, prototyping or evaluation. But in the end, we’re all doing the same thing: picking and placing components on bare substrates. (Company white paper; circuitsassembly.com/cms/white-papers)

PCB Assembly “New Product Introduction” Authors: ASM Siplace Abstract: This new publication presents solutions for everyday challenges, lots of tips and tricks, and a convenient checklist for the NPI process. It is directed toward manufacturers that want to implement robust NPI processes in their high-mix electronics production environments with consistent tool chains in order to raise the efficiency and quality of their new product introductions. Readers will learn how even the first yield can be produced efficiently and error-free despite faulty Gerber data, incomplete bills of material, and missing or late component descriptions. (Company white paper; circuitsassembly.com/cms/white-papers)

Plating “Electrochemical Cell Geometry for Uniform Processing of Printed Circuit Boards” Authors: S.T. Snyder, H.M. Garich, B.S. Kagajwala and E. J. Taylor; This email address is being protected from spambots. You need JavaScript enabled to view it.. Abstract: An electrochemical cell geometry based on a novel flow mechanism for uniform processing (metallization or electroetching) of PCBs is described. This unique flow scheme utilizes eductors, coupled with dampening elements and flow channels to enable a non-impinging flow scheme that results in uniform boundary layer thickness and consequent uniform current and thickness distribution over a full-size printed circuit board panel (18×24 in.). This tank has been extensively characterized for thickness distribution under direct current plating conditions and compared with commercial plating cell geometries that utilize both eductor flow and/or air sparging agitation. Uniformity data, along with plating results of varying printed circuit board feature sizes, are also presented. (Products Finishing, August 2012)

“Immersion Gold: Why More is Not Better” Authors: Hank Lajoie and Trainor; This email address is being protected from spambots. You need JavaScript enabled to view it.. Abstract: The nature of immersion gold is to attack the electroless nickel, remove it and replace it for the benefits that gold can offer. This activity of gold can defeat the intent for its use and supports the approach, starting with gold is good, so more must be better. The ENIG process has been challenged with this “more is better” concept. The ENEPIG process attempts improvement with protecting the EN from the gold. The dynamic chemistries involved within the process require close control and proper balances of ingredients. The effects of some of these contaminations and process imbalances can be exacerbated through ignorance and neglect of process control and pursuing the “more is better” approach. Experience with these dynamics of the electroless nickel, electroless palladium and immersion gold have offered improved and robust chemistries that fit with practiced process controls and can realize the value of gold without the “more is better.” Effects of commonly encountered bath contaminations from materials, process environment and process controls are presented to illustrate the immersion gold impact on the electroless nickel that can lead to defects. (SMTA International, October 2012)

Soldering “Overcoming Head-in-Pillow Defects in Hybrid LGA Socket Assembly” Authors: Marie Cole, et al; This email address is being protected from spambots. You need JavaScript enabled to view it.. Abstract: The processor card of a new midrange server system has a unique large mass SMT connector system that requires use of a vapor phase reflow. In addition, the board contains four ball grid array connectors, known as hybrid LGA sockets, to accommodate plugging of LGA processors. Due to the large size of these BGA sockets, which makes them vulnerable to dynamic warpage and other physical changes during Pb-free processing, solder joints in the connector array may be more susceptible to the formation of HiP defects. This paper discusses optimization of the assembly process for this complex PCBA. Several design of experiments were evaluated, including solder paste chemistry, stencil parameters, vapor phase reflow profile settings, reflow SMT pallet and fixture designs. Additionally, characterization of the contribution of incoming connector tolerances and thermal dynamic warpage was considered, along with various reliability evaluations related to this type of head-in-pillow defect. (SMTA International, October 2012)

This column provides abstracts from recent industry conferences and company white papers. Our goal is to provide an added opportunity for readers to keep abreast of technology and business trends.

What is the downstream payback, and how will it inform solar use?

For the most part, this column has concentrated on technologies and processes used to raise the efficiency and lower the cost of photovoltaic (PV) cells. But have you thought a bit further downstream as to what that may mean in terms of how the cells will be used, the payback and, ultimately, the value to the homeowner? I’m guessing that a large percentage of you have not! (Come on, admit it.)

We are often so focused on a certain element of solar technology, that the bigger picture is overlooked. So, this month I thought it would be interesting to provide a general overview of residential PV systems – from installation to ROI to cell efficiency benefits to common myths. Perhaps after reading this, your roof will soon be the proud owner of some solar panels. The PV system and how it works. Understand the distinction between on-grid (or grid-connected) and off-grid (or non-grid-connected). On-grid systems are most common in areas of high population density and have connectivity to a local power supply. During peak/daylight hours, the homeowner draws what they need from the PV system and feeds the “extra” electricity generated into the national grid, for which there is a payout based on local Feed-in-Tariff rates. During the dark/off-peak hours, the homeowner draws power from the national grid. There are four main components to an on-grid system:

Solar modules (panels), made up of roughly 60 crystalline-silicon (c-Si) solar cells each.

Inverter used to convert the power from direct current (DC) to alternating current (AC) used by household appliances. (Note: Inverters may need periodic replacement, as they may not last as long as the panels.)

Regulator for voltage stability.

Meter to monitor the quantity of power the PV system is pushing to the national grid, so the homeowner can be compensated. A home that is completely off-grid is one that does not have easy accessibility to the nearest grid line. These systems are more popular in remote areas, where it is simply too expensive to provide the cables necessary to connect to the national power grid. In this case, the homeowner would have all the same components as the on-grid system, as well as:

Deep cycle lead-acid batteries that can withstand many deep discharge and recharge cycles.

A charge controller to ensure batteries receive the optimum charging voltage.

The batteries store power generated during daylight/peak hours, and the homeowner draws from the battery surplus in off-peak periods. Because of the battery requirement for off-grid systems, the investment is significantly greater than that of an on-grid system.

How many panels, how much power, what’s the cost and payback? Obviously, the quantity of panels required for a residential installation is dependent on a number of different factors, including the size of the home, average power consumption rates, orientation (sun facing or not) of the residence, roof tilt, on-grid or off-grid configuration and Feed-in-Tariff rates. Solar panels/modules are most commonly fabricated from approximately 60 c-Si solar cells, with each panel producing 200W to 250W peak. Anywhere from 12 to 15 panels are required to deliver a typical 3kWp system, which, generally speaking, will power a modest-size home (2000 – 2500 sq. ft.). Of course, if you have the roof space and the budget, a higher power system may also be appropriate. Using a typical English home as an example, one could purchase a budget/lower-end installation for a cost of around $9,400 or a deluxe/higher-end system for approximately $17,200.

With a modest solar PV panel installation (3kWp) positioned on an optimum roof configuration (south facing with a 30˚ tilt) in Birmingham, England, that was registered for the UK’s Feed-in-Tariff before Dec. 12, 2011, the homeowner could receive and save:

Annual tariff income generated: $1,600.

Annual fuel bill savings: $120.

Total income and savings: $1,890.

Projected net profit over 25 years: $27,700.

Expected time for full return on investment: 8 to 9 years for a $15,670 3kWp system.

On the other hand, if the homeowner were to have installed the same system and registered for the Feed-in-Tariff after Apr. 1, 2012, at the current, lower rate, the same scenario would result in the following:

Annual tariff income generated: $830.

Annual fuel bill savings: $120.

Total income and savings: $1,010 per year.

Expected net profit over 25 years: $7,580.

Expected time for full return on investment: 15 to 16 years for a $15,670 3kWp system.

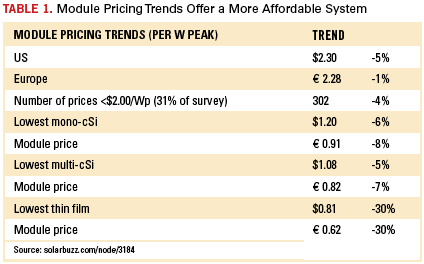

These examples certainly illustrate the massive impact that Feed-in-Tariff rates have on payback time and the effect that has on solar system adoption. Certain countries (read: Germany and Italy) had huge incentives for many years, making them the solar installation centers of the universe. With those subsidies now reduced, installations have slowed significantly. But, it’s not all bad news for solar. Solar system prices have simultaneously fallen dramatically due to several factors, the most significant of which is reduced incentive levels. In fact, the average cost of Chinese Tier-2 crystalline PV modules1 dropped to $0.96 per watt in January, representing an annualized price shift decline of 22%. So, while incentives may be lower, so are module costs (Table 1).

The efficiency equation. On the cell manufacturing side, there is a clear shift toward more efficiency, as opposed to more capacity. Instead of churning out average-rated 14% efficiency cells, there is certainly a move toward hitting the 18% to 19% efficiency mark, despite the higher cost. Obviously, the view is that more efficient systems will deliver a greater payback (fewer modules needed for the same energy generation), and, though the difference is slight at the moment, a more significant cost benefit is projected for the long-term.

The various technologies discussed previously in this column, such as print-on-print, rear-side passivation, MWT and selective emitter, all combine to substantially improve cell efficiency, thereby generating more power and ultimately lower the cost over the life of the system.

Solar fact or fiction. There are numerous myths about solar and its use as an alternative energy source, so I thought I’d take this opportunity to dispel a few.

Myth: “The energy required to make solar panels is greater than all the energy those panels will ever produce.”

Reality: The energy delivered over a 25-year period by a roof-mounted solar system in Central Northern Europe is roughly five times that of the energy required to make the panel.

Myth: “Solar panels work just as well when it’s cloudy.”

Reality: Solar panels will still work when it’s cloudy, but many of them will only produce 10% to 20% of their peak power. Before buying, it’s worth comparing the low light level performance of various panels. The panel datasheets usually show power graphs at several different light levels, ranging from the normal solar standard of 1000w/m2 to 250w/m2.

Myth: “Solar technology is improving so quickly that it must be better to wait before I buy.”

Reality: Small advances in cell efficiency do occur each year, but many countries are also reducing their Feed-in-Tariffs, so waiting may mean missing out on a good deal. Module prices are falling, so from that point of view, it may be worth waiting. But, for the overall cost of ownership, the Feed-in-Tariff is the real metric, and the longer you wait, the more likely this incentive will be lower.

Is there solar in your future? There’s no doubt that the solar industry is going through a bit of a reset at the moment, but for the long-term it is one of the most affordable and effective energy technologies and is no doubt here to stay. The majority of solar modules are guaranteed for 25 years and, at current Feed-in-Tariff rates, most homeowners realize complete ROI well before any modules need to be replaced. As new technologies continue to improve cell efficiencies, solar will only become an even better investment.

Tom Falcon is a senior process development specialist at DEK Solar (dek.com); This email address is being protected from spambots. You need JavaScript enabled to view it.. His column runs bimonthly.

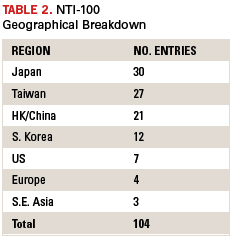

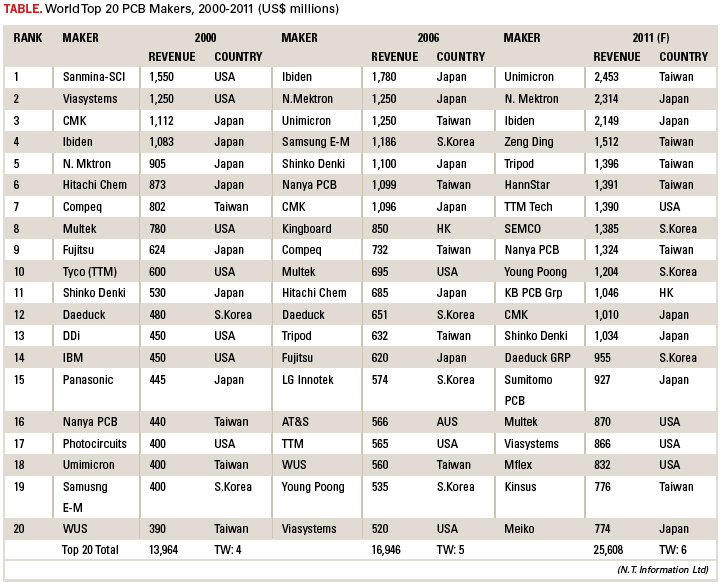

The 104 manufacturers on the 2011 NTI-100 made up more than 80% of the world’s PCB output.

The NTI-100 list for 2011 was greatly influenced by exchange rates. Taiwanese fabricators continued to make gains, followed by Japanese manufacturers. Some names disappeared because they were purchased; their sales are included in the acquiring firm’s results. Some disappeared because they did poorly. Several fabricators, particularly Japanese firms, made it because of exchange rates.

As usual, the author is not almighty and is certain that there are many errors. Some companies that should be on the list may be missing. He assumes full responsibility for any errors. He wishes to express his gratitude to those PCB makers that provided him valuable data.

Exchange rates. Currency values played a role in certain companies’ performance. Table 1 lists the average exchange rates of major currencies against the US dollar.

Assumptions. All acquisitions that took place during 2011 are assumed to have taken place on Jan 1, 2011. In the cases of flexible circuit manufacturers (FPC), the assembly value is included because it is extremely difficult to separate bare board sales from total revenues. Therefore, the rankings are relative, not absolute. Finally, a large portion of revenues of Taiwan, Japanese and US makers comes from overseas operations, and therefore involves double conversions. The author has no knowledge of what exchange rates Taiwanese makers, for example, used to convert output in RMB into NT dollars to report consolidated revenues.

Entries by country or region. There are 104 companies on the 2011 NTI-100 list. There are more Japanese makers than Taiwanese because of a 10% increase from 2010 to 2011 in value of the Japanese yen against the US dollar. Several Japanese makers would not have made it had the 2010 exchange rate remained constant.

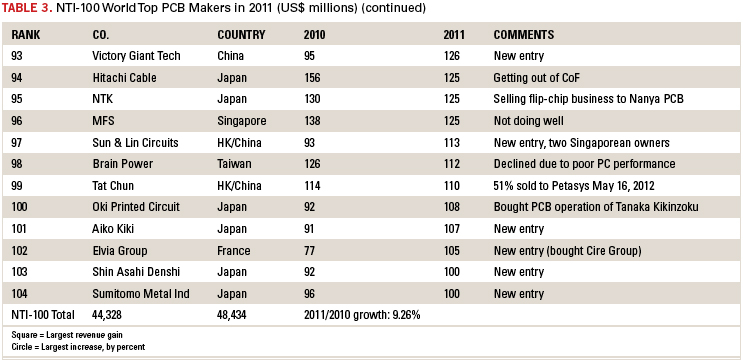

Table 3 lists the 2011 NTI-100. Although comments are included in the table, more extensive comments on certain fabricators are below.

Unimicron. Unimicron purchased Ruwel International of Germany and Clover Electronics of Japan in 2011 and took in partial revenues of these two into its fiscal 2011 revenue. The revenue in the table takes into consideration full-year accounts of Ruwel and Clover. Unimicron is rumored to be shutting one of its Shenzhen facilities (“Plato”). It plans to build new facilities in Jining in Shandong Province and Nantong along the Yangtze River, north of Shanghai. Its 2011 output in China jumped by 60%.

Nippon Mektron. Its subsidiary, Mektec Suzhou, obtained water permission for its long-awaited second plant, which is undergoing construction. It is scheduled to commence operations in the fourth quarter this year. Its Thai subsidiary, Mektec Thailand, flooded badly, but most of the equipment was moved to higher floors and saved. It could restart production as early as December, and become fully operational by March. The company is expected to reach $3 billion in revenue in fiscal 2012. Ibiden. Ibiden did poorly in flip-chip substrates for MPUs in 2011 due to sluggish PC shipments, but did very well with buildup MLBs for smartphones and tablets. It did well with IC substrates for baseband chips used for smartphones and tablets. It is reported that Ibiden is investing more than $2 billion to expand its overseas operations over the next three years, of which two-thirds will be used for PCB expansions. One-third of its fiscal 2011 revenue came from overseas production, but in fiscal 2013, Ibiden seeks to generate 60% of its revenue from overseas operations, particularly the Philippines and Malaysia. Its flip-chip substrate business is tops in the world, despite the slower 2011.

Zhen Ding. Zhen Ding is a business unit of Foxconn and was called Foxconn Advanced Technology prior to its Dec. 26, 2011, listing on the Taiwan Stock Exchange. A large portion of its revenue is said to come from FPC and FPC Assembly. The largest customer of its FPC business inclusive of FPC Assembly is said to be Apple Computer. It aims to become the largest PCB maker in the world in a few years, according to recent remarks by its CEO. It operates at two locations in Shenzhen, one at Yinkou, one at Qinghuangdao and one at Huai’an, all in China. Zhen Ding sold its Yantai facility to a business unit of Foxconn called Pan International prior to the stock listing because it was losing money, according to industry sources.

Tripod. Tripod’s revenue fell slightly in 2011 in terms of NT dollars due to poor PC demand. It has been reducing its dependency on the PC sector and diversifying its end-product markets. It is building new plants in Xiantao, about 100km west of Wuhan, along the Yangtze River. Two manufacturing buildings (of four planned) are nearly finished, and one will begin equipment installation toward the end of the third quarter and commence operations partially in the first quarter 2013. Automotive PCB is increasing at Tripod.

HannStar Board. HannStar Board completely absorbed GBM’s PCB units (GBM Yuanmao, CMK-GBM and GBM Chuangyi). GBM was building a facility in Chongqing. HannStar Board is trying to reduce its dependency on the notebook motherboard business. It made 93 million NB motherboards in 2011, mostly six and eight layers.

TTM Technologies. TTM is said to be strengthening its buildup MLB production capability both in technology and volume by adding a number of advanced laser drilling machines. Its US side of the business seems to be holding steady. Given the amount of investment in China, TTM’s future growth will come mainly from Chinese operations (TTM Asia Pacific, the former Meadville Technology).

Semco (Samsung Electro Mechanics Co). Semco benefited from high demand for Galaxy smartphones and tablets made by Samsung Electronics. However, 70% of its revenue came from IC substrates, flip-chip and wirebond types. Its Kunshan subsidiary, which makes buildup MLBs, also made a small contribution. In 2012, Semco is aiming at 1,900 billion won in revenue ($1.73 billion at 2011 exchange rates).

Nanya PCB. About $400 million of Nanya PCB’s revenue was derived from its Kunshan subsidiary, which has almost finished construction of a four-story PCB Plant 3 intended for wirebond IC substrates and for buildup MLBs. Nanya seems to be doing poorly in the first half of 2012, with a revenue decline of about 20% compared to the same period last year (parent only). Expected gains in the second half will hopefully compensate for a weak first half.

Young Poong Group. YP Group consists of Korea Circuits, Terranix, Interflex (FPC) and Young Poong Electronics (FPC). The combined FPC revenue of Interflex and Young Poong Electronics was $722 million, fourth largest in the world after Nippon Mektron, Sumitomo Denko Printed Circuits and M-Flex. Interflex’s gigantic eight-story building is completed in Ansan City, Korea, next to the head office of Korea Circuits. This plant will contribute greatly to the future revenue growth of YP Group. Buildup MLBs made by Korea Circuits are sold mainly to Samsung Electronics.

KB PCB Group. Kingboard Chemical’s PCB group consists of Elec & Eltek, Techwise, Evertek, Glory Faith, Top Faith and Express Circuits. Due to rising material costs and stiff price competition in the market, KB’s revenue was slightly below that of 2010. However, KB is in expansion mode, building huge plants for Elec & Eltek in Yangzhou (north of Nanjing), whose total production capability is planned to be 10 million sq. ft. per month when all five buildings are finished. Evertek in Kunshan is planning a four-story plant for buildup MLBs. Elec & Eltek Thailand was spared from the flooding last year. Top Faith seems to be building a new facility in Qingyuan, Guangdong Province.

Shinko Denki Industry. One of the major flip-chip package substrate makers (with Ibiden, Nanya PCB and SEMCO) for Intel chips, Shinko Denki, is building a major substrate plant in the city of Takaoka, Nagano Prefecture, for next-generation chips.

CMK. CMK’s revenue fell 10% in Japanese yen, but thanks to the rising yen, it remained in the NTI-$1B Club, which had 13 companies in 2011, up two from 2010. CMK was the largest automotive PCB maker in 2011, with revenue of $530 million, well ahead of No. 2 Viasystems. It expects that 60 to 65% of its revenue this year will come from automotive applications.

Daeduck Group. Daeduck Group consists of Daeduck Electronics and Daeduck GDS. Daeduck Electronics has two subsidiaries: APERIO, a maker of IC substrates, and Daeduck Electronics Philippines. GDS has a plant in Tianjing, which is rumored to be shut down. Its major customer is Samsung Electronics. Samsung is planning to ship 420 million cellphone units in 2012, of which 190 are to be Galaxy smartphones. Daeduck will benefit from this and is likely to join NTI-$1B Club in 2012.

Sumitomo Denko Printed Circuit. Several “Sumitomos” are engaged in the manufacture of PCBs: Sumitomo Mining (through a subsidiary, Shinko Mfg), Sumitomo Bakelite, Sumitomo Cable, Sumitomo Metal Electro Device and Sumitomo Denko. Sumitomo Denko has two FPC plants in Japan, two in China and one in Vietnam, about to be increased to two since it will be purchasing Sumitomo Bakelite’s Hanoi plant at the end of the third quarter. Forty-five to 50% of Sumitomo Denko’s revenue is said to come from sales to Apple.

Multek. Multek is a part of Flextronics and operates five plants in Zhuhai, China, one in Boeblingen, Germany, one in Sãn Paulo, Brazil, and one in Northfield, MN. Its FPC and rigid-flexible output seems to be increasing steadily, as is its high layer-count MLBs. Multek is a major buildup MLB maker in the world.

Viasystems Group. Some 48% ($412 million) of Viasystems’ bare board revenue came from automotive PCBs. It acquired DDi in May 2012, which will boost its military PCB output by several times. Its prorated revenue for bare PCBs in 2011 was $1.129 billion. Viasystems is one of the major high layer-count MLB manufacturers.

Multi-Fine Line Electronix. M-Flex sold its headquarters in Anaheim, CA, to DDi, which is now a Viasystems division, and moved to a new building in Irvine, CA. It used to have close to 400 employees in Anaheim, but is said to have only 50 now, with all other employees in China (Suzhou and Chengdu). Several years ago, over 80% of its revenue was from sales to Motorola. Now, more than 90% of its revenue comes from five major customers, including Apple and RIM.

Kinsus Technology. Kinsus Suzhou’s revenue contribution was next to nothing in 2011, but will be substantial in 2012, as its package substrate operations have been ramping since the beginning of 2012. Included in Kinsus’ revenue are sales from Piotek, formerly Boardtek, a subsidiary of Asustek. Kinsus PCB Group now belongs to Pegatron, a manufacturing arm of Asustek.

Meiko Electronics. Meiko sustained triple punches in 2011. The March earthquake/tsunami destroyed Meiko’s Ishinomaki plant, and the Fukushima plant was shut down for several months due to its proximity to the Fukushima nuclear plant, which exploded from the loss of its cooling pumps. Then, on Oct. 18, one of its two Wuhan plants was shut down for three months by Chinese authorities on suspicion of wastewater treatment violations, which was very much a political issue related to Apple’s suppliers (the “poison Apple” case, as the Chinese called it). The issue was resolved on Jan. 19, 2012. As a result, Meiko has been accelerating operation of its new Hanoi, Vietnam, plant. Despite all these problems, Meiko ended fiscal 2011 with a net profit. Meiko will see strong growth in 2012, with the Fukushima and Wuhan plants operational and the new Vietnam plant contributing greatly.

Compeq. Compeq has been doing well this year. It is one of the major PCB suppliers to Apple for all product lines (iPhones, iPods, iPads and iMac). Its Chongqing buildup MLB plant is scheduled to commence operation in the first quarter 2014.

Wus Group. Wus China was listed on the Shenzhen Stock Exchange in 2010. This China organization is separate from its Taiwan operation, but major ownership is common to both organizations. A new plant consisting of two buildings in Kunshan, about 20 minutes from the existing plant, is nearly completed, with total floor space of 2 million sq. ft. A second plant is in planning at Huangxi, 100 km east of Wuhan. Wus is one of the major high layer-count MLB makers in China. Of the $468 million revenue generated at Kunshan, well over $100 million came from MLBs above 18 layers.

AT&S. AT&S is Europe’s largest PCB maker, but the majority of its output came from its Shanghai plant ($403 million, or 56%). AT&S is also a major producer of automotive PCBs, with 2011 revenue of $120 million. It has been building a gigantic buildup MLB plant in Chongqing since July of 2011, and the building seems almost complete. It is scheduled to commence operation in early 2013. AT&S took a technical license from Panasonic to manufacture “ALIVH” products.

Fujikura. Fujikura is a major FPC manufacturer. Unfortunately, 95% of its output came from three plants in Thailand, two of which were completely flooded in fall 2011. One of the plants started partial operation in May, and the other is scheduled to restart operation in December, according to the company’s annual report. In the meantime, Fujikura purchased an FPC plant in Vietnam from bankrupted Sakai Denshi last December and commenced operation in January. At the same time, Fujikura selected land in Thailand high above sea level to build a new flex manufacturing plant, which is supposed to generate 30% of future revenue.

Gold Circuit Electronics. GCE is the second largest notebook motherboard maker, after HannStar Board. Unfortunately, its main notebook motherboard plant in Changzhu, China, had a fire and was disabled for some time. It has been restored.

Simmtech. Simmtech used to be Chungbuk Electronics. When it started to enter the single-in-line memory module business, it changed its name to Simmtech. In the last several years, Simmtech has been growing rapidly in the IC substrate market as well. It built a plant in Xian, China, to supply memory module circuits to Micron and Samsung Electronics.

Nitto Denko. Nitto Denko is a major Japanese FPC maker with plants in Japan, China (Suzhou) and Vietnam (near Ho Chi Minh City). It is building a new plant next to the existing plant in Vietnam.

Chin Poon Industrial. Chin Poon has several plants in Taiwan and a plant with two buildings in Changshu, China. It is the third largest automotive PCB maker in the world, with $300 million automotive revenue. Its Thailand subsidiary (minority share) was badly damaged by the flooding in the fall of 2011, but is fully restored.

Unitech Electronics. One of the largest buildup MLB makers in the world, Unitech built a new buildup plant in Ilan, Taiwan, which started operation in 2011. It has a provision to build a plant near Nanjing, but no concrete plan is set at this time, it seems. PID (Panasonic Industrial Devices). Formerly Panasonic Electronic Devices, and inventor and licensor of ALIVH technology, PID built a second ALIVH plant in Taiwan (Tayuan) and another ALIVH plant in Vietnam (Hanoi). Its overseas ALIVH production capability will triple when these two new plants become fully operational this year.

LG Innotek. It is said that LG Innotek supplies over 80% of its output to its parent, LG Electronics. Since LGE did poorly in cellphones in 2011, LG Innotek also did poorly. It decided to exit the high layer-count MLB business in 2010, which is a shame because it had very high technology in this field. The reason for the exit is that the market for high layer-count MLBs is rather small and is not growing compared to other fields such as IC substrates and buildup MLBs. So, now, LG Innotek concentrates on IC substrates and buildup MLBs. It supplies buildup MLBs (“any layer” type) for Apple’s smartphones.

Founder Technology. Owned by Beijing University, Founder Group went into the PCB business in 2004 when it purchased Zhuhai Multilayer. Since then, it acquired a quickturn and prototype maker in Hangzhou and built two new PCB plants: one in Zhuhai and the other in Chongqing. Zhuhai “Fushan Branch” plant in Doumen district of Zhuhai consists of four operations: buildup MLB, QTA and prototyping, R&D and IC substrate. The last operation is called ACCESS (Advanced Chip Career Electronic Substrate Solutions). ACCESS is a JV between Founder and Israeli substrate maker Amitek. (ACCESS’ revenue – $70 million in 2011 – is not included with Founder’s.) Founder built its second buildup MLB plant next to its existing site early this year and a separate quickturn plant at its Zhuhai Fushan Branch last year. Founder is one of what the author calls “three musketeers of China,” the others being CCTC and Shennan Circuits.

Shennan Circuits. A division of AVIC Group (Aviation Industry of China), which makes jet fighter airplanes, helicopters, automobiles, missiles and jet engines among other things, Shennan Circuits is one of the China’s best high layer-count MLB builders, with two plants in Shenzhen (Nanshan and Longgang districts). In 2011, it commenced production of BGA substrates and has been negotiating with Wuxi government to build a new BGA plant there.

China Circuit Technology Corp. CCTC is one of the large makers of buildup MLBs for local cellphone makers. CCTC has two plants in Shantou, Guangdong Province, a small plant in Shenzhen and another small one in Shichuwan Province. CCTC belongs to Go-World Group, which also has a laminate manufacturing subsidiary.

DDi. DDi, the second-largest PCB maker in North America after TTM, was purchased by Viasystems Group in May. This purchase boosts Viasystems’ military portion of its PCB business to well over $100 million.

Wuzhu Group, Shenzhen Fast Print, Shenzhen Sun Tak and Bomin Electronics. These three makers may be called second tier “four musketeers of China.” All have substantial expansions ongoing in various parts in China: Wuzhu in Dongguang, Fast Print in Yixing, Suntak in Jiangmen and Bomin in Meizhou.

Tat Chun Circuits. Some 51% of Tat Chun was acquired by Korean high layer-count MLB maker ISU Petasys in May of this year. “ISU” in Korean means “Pear Tree, or 梨樹. Peta is 10 to the 12th. The parent company, ISU Chemical, named it as Petasys to wish that it would grow to “infinity.” Tat Chun has had a business alliance with Japan’s Toppan-NEC, a competitor of ISU Petasys for Cisco’s programs. ISU Petasys is the largest supplier to Cisco. What is going to happen with Tat Chun, Toppan-NEC and ISU Petasys is beyond this author’s imagination. Good luck to all parties involved.

Ed.: For a larger version of Table 3, right-click on each table, then click View Image and increase the size.

If readers have questions about other NTI-100 entries, the author would be happy to respond.

One final comment: The “80-20” rule normally applies to the amount of market share controlled by 20% of the manufacturers in the same field. It is estimated that there are 2,600 to 2,800 PCB companies in the world today. The 104 companies on the NTI-100 list represent 3.7% of the total. The total revenue ($48 billion) of these 104 makers accounted for 81% of the world output ($59 billion). Therefore, in the PCB field, the rule may be more like “90-10”; that is, the big get bigger and faster.

Once a PCB manufacturer’s revenue reaches a certain level, say, $500 million per annum, it must keep running, meaning continuous investment. Some companies are taking a different path, specializing in a niche market with niche products. Which is better?

Printed circuit boards are a critical commodity. Here’s how to treat them as such.

Electronics quality and reliability are highly dependent on the capabilities of the manufacturer. Manufacturing issues are one of the top reasons companies fail to meet warranty expectations. These problems can result in severe financial pain and loss of market share. What a surprising number of engineers and managers fail to realize is that focusing on processes addresses only part of the issue. Supplier selection also plays a critical role in the success or failure of the final product.

Designing printed circuit boards today is more difficult than ever due to significantly increased density, higher lead-free process temperature requirements and associated changes required in manufacturing. Many changes have taken place throughout the entire supply chain regarding the use of hazardous materials and the requirements for recycling. The RoHS and REACH directives have caused many suppliers to the industry to change their materials and processes. Everyone designing or producing electronics has been affected.

PCBs should always be considered a critical commodity. Without stringent controls in place for PCB supplier selection, qualification and management, long-term product quality and reliability are neither achievable nor sustainable. Here, we discuss some best practices and recommendations for improving your PCB supply chain.

First, create a PCB commodity team with at least one representative each from design, manufacturing, purchasing and quality/reliability. The team needs to meet on a regular basis to discuss new products and technology requirements in the development pipeline. These meetings can take place through conference calls or via onsite visits. Pricing, delivery and quality performance issues with existing PCB suppliers should be reviewed. The team is also responsible for identifying new suppliers and creating supplier selection and monitoring criteria.

Second, establish initial PCB supplier selection criteria. The criteria should be unique to your business and products, but some general selection criteria include:

Time in business.

Revenue.

Growth.

Employee turnover.

Training program.

Certified to standards you require (IPC, MIL-Spec, ISO, etc.).

Capable of producing the technology you need as part of their mainstream capabilities.

Don’t build in process “niches” where suppliers claim capability, but little volume is built there.

Have quality and problem-solving methodologies in place.

Have a technology roadmap.

Have a continuous improvement program in place.

Ideally, the suppliers demonstrate long-term stability from both quality and business perspectives. Multiple factory locations and risk mitigation programs can further protect against catastrophic political and weather-related events. After this initial screening, visit the PCB suppliers that seem to be appropriate matches. Site visits to the actual fabrication facility by personnel knowledgeable in PCB fabrication techniques are crucial. The site visit is the best opportunity to review process controls, quality monitoring and analytical techniques, storage and handling practices and conformance to generally acceptable manufacturing practices. It is also the best way to meet and establish relationships with the people responsible for manufacturing your product.

After choosing some potential PCB suppliers, the true qualification work begins. Qualifying a PCB supplier is always a two-step process. The first step is to qualify both a design and the PCB manufacturer through rigorous product and test-vehicle-based evaluations. The PCBs built for qualification should be evaluated to the standards you require by both the PCB supplier and your company (or an independent lab). The second qualification step is to initiate ongoing testing to monitor outgoing quality through a combination of test vehicle and lot qualification.

How do you verify a PCB supplier is capable of meeting your reliability requirements? There are currently six common methods for testing and qualifying PCBs:

Modeling and simulation.

Cross-sectioning combined with solder float/shock tests.

Thermal shock testing (also

thermal cycling).

Printed Board Process Capability, Quality, and Relative

Reliability (PCQR2).

Interconnect stress testing (IST).

Highly Accelerated Thermal

Shock (HATS).

Very early in the design cycle, software simulation and modeling can be performed. As an example, DfR has implemented IPC-TR-579 into an automated design analysis software called Sherlock to permit rapid assessment of basic PCB robustness. IPC-TR-579 documents a “Round Robin Reliability Evaluation of Small Diameter (<20 mil) Plated Through Holes in PWBs.” This activity was initiated by IPC and published in 1988.

The objectives were to confirm sufficient reliability, benchmark different test procedures, evaluate influence of PTH design and plating, and develop a model. Some advantages of the IPC-TR-579 model are that it is analytical, validated through testing, and comments on the relative influence of design and material parameters. However, the validation data are over 18 years old. The model is unable to assess complex geometries, and it is difficult to assess the effect of multiple temperature cycles. The model also uses simplified assumptions (linear stress-strain above yield point). Finally, the model does not account for the effect of via fill and does not consider other failure modes such as knee cracking and wall-to-pad separation.

To successfully model a PCB design, the first step is to define the environment (Figure 1). Test, field or both environments can be modeled.

The second step is to upload the actual design information. Thermal maps can also be imported, if appropriate. The third step is to select the laminate and prepreg material. With this information, the stackup and copper percentage are automatically identified. Then, the PTH fatigue analysis can be performed.

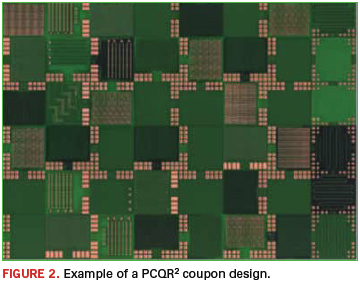

Another method is to qualify the design and manufacturer through the PCQR2 database and program. The program consists of a coupon design, a test standard, and a database of participating suppliers. The coupon has an 18" x 24" layout with 352 1" x 1" test modules (Figure 2). It can consist of two to 24 layers (rigid, rigid-flex) and requires builds of three panels and three non-consecutive lots with six times simulated assembly and HATS cycling.

An advantage of the PCQR2 program is that it is available in an industry standard (IPC-9151) format. It is easy to follow and provides real data for understanding PCB supplier capabilities (Table 1). It also provides a comparison to the rest of the industry through the use of an anonymous database. However, it is an IPC-approved monopoly and can be expensive, ranging from $2,000 to $5,000, not including panel costs, per supplier and facility evaluated.

Interconnect stress testing (IST) is the overwhelming favorite of high-reliability organizations for lot-based qualification testing. IST uses small (1" x 4") coupons that can fit along the edge of a product panel. Testing is automated, widely used and has the ability to drive barrel fatigue and post-separation failures. The large number of holes (up to 300) and continuous resistance monitoring make it far superior to cross-sectioning. And, in most cases, IST is a more cost-effective option. There are some potential issues to be aware of, however. The IST coupon design is critical. Preconditioning, test frequency, maximum temperature and failure requirements must all be specified. Test frequency can range from every lot to every month to every quarter. Maximum temperatures of 130˚, 150˚, and 175˚C are most commonly used. And, different markets and organizations specify different times to failure, with 300, 500, and 1000 cycles most common.

Next, if your product line ranges from simple to highly complex, consider tiering (low, middle, high) suppliers. Tiering permits strategic supplier selection to maximize cost savings and quality against your product design requirements. Match supplier qualifications to the complexity of the product. Some criteria for tiering suppliers include:

Finest line width.

Finest conductor spacing.

Smallest drilled hole and via.

Impedance control.

Specialty laminates or construction needed (PTFE, flex, mixed technologies).

Buried resistance or capacitance.

Use of HDI, microvias, blind or buried vias.

Minimize use of suppliers that outsource critical areas of construction. Again, do not exist in the margins of any supplier’s process capabilities.

Relationship management is another important element of success. Ideally, you are a partner with your PCB suppliers. This is especially critical if you have low volumes, low spend, or high technology and reliability requirements. Good partnering practices include:

Routine conference calls between your PCB commodity team and each PCB supplier’s equivalent team.

Quarterly business reviews (QBR) that review spend, quality, and performance metrics, and also include “state of the business updates.” Business updates can address any impending changes, such as factory expansion, move, or relocation, critical staffing changes, new equipment/capability installation, etc. The sharing is done from both sides. You also share any data that would help strengthen the business relationship: business growth, new product and quoting opportunities, etc. At least once per year, the QBRs should be site meetings that alternate between your site and the supplier factory. The factory supplier site visit can double as the annual onsite visit and audit that you should be performing.

Ongoing supplier “lunch and learns” or technical presentations held at your facility or via webinar. Suppliers routinely provide education regarding their processes and capabilities. They can educate your technical community on PCB design for manufacturing, quality, reliability and cost factors. They can also inform you on pitfalls, defects, and newly available technology. This activity is usually performed free of charge, and suppliers may even provide free lunch to encourage attendance. It also gives you an opportunity to educate them on your needs.

Supplier scorecards should exist and be used on a rolling quarterly and yearly basis. Typical scorecards include both objective and subjective metrics. Objective metrics include on-time delivery, cost, PPM defect rates, and quality excursions, which require root cause corrective actions. Subjective measures include communication issues (speed, accuracy, responsiveness to quotes) and cost-savings suggestions. And, there should be detailed discussion of any recalls, notifications or scrap events exceeding a certain threshold.

Finally, make sure that any supplier has a robust continual quality improvement program in place. At a minimum, consider monitoring and reviewing the top three PCB factory defects, process control and improvement plans for those top defects, yield and scrap reporting for your products and feedback on general issues facing the PCB industry.

The foundation of a reliable product is a reliable PCB. Having a comprehensive strategy for selecting and qualifying PCB suppliers ensures the foundation is strong.

Cheryl Tulkoff is senior member of the technical staff and Craig Hillman, Ph.D., is CEO and managing partner of DFR Solutions (dfrsolutions.com); This email address is being protected from spambots. You need JavaScript enabled to view it.. DFR will be exhibiting in September at PCB West 2012 at the Santa Clara (CA) Convention Center.

The Japanese Ministry of Economy, Trade and Industry (METI) released June’s production data for the electronics industry in Japan last week. Now that a snapshot for the first half is available, we can review a few market trends and assess our plans for the remainder of the year.